"I'm happy being paid in Australian dollars for the next 10 years," he said, noting that "the Australian economy is being punished for its virtue".

AUSTRALIA has joined the CASSH economy and it's good news for inbound investment, according to Blackrock's global chief investment strategist Russ Koesterich. He named Canada, Australia, Singapore, Switzerland and Hong Kong as developed countries whose economies had performed well through the global financial crisis.

"You can also include New Zealand and Norway but I couldn't work out where to put the letters," joked Mr Koesterich, who ranks those countries alongside lower-cost developing countries as a likely target for global investors.

He particularly likes their low gross public debt and the fact in all of them fiscal deficits averaged less than 1 per cent in 2010, as against an average of 7.5 per cent in Europe, the US and Japan.

But he's not so keen on the US, he says, because of the likely dampening effects of fiscal drag, where more people are going to find themselves paying higher rates of tax, as their earnings recover, to help reduce the country's massive sovereign debt.

"Some of the near-term risks have shifted from Europe to the US," he said, noting the US probably would be "more resilient than the UK but growth in the US may disappoint because of drag".

Two area of surprise in the US-based expert's presentation this week were that he didn't expect a bust in the US bond market despite the very low yield of Treasury bonds and he didn't expect the Australian dollar to lose much ground even after the US Federal Reserve stopped its quantitative easing program.

"I'm happy being paid in Australian dollars for the next 10 years," he said, noting that "the Australian economy is being punished for its virtue".

He said quantitative easing would cease only when the US labour market improved, "and that could be a multi-year process ... say as long as five years".

"The Fed's policy is basically unlikely to change until we see an improvement in the global economy and when that happens there will be a limited negative effect on the Australian dollar."

He said US Treasury Bonds were and would remain an investment target for central banks and institutions worldwide.

"They're tools of monetary policy rather than genuine investments," he said. "Buyers are not really looking for return."

He did warn that many markets, including Australia, had sharemarkets that had run hard and that "emerging markets have more compelling valuations".

But he's not writing off Australia, not only because of the solid international interest in our equities but also because "Australia's low debt will allow for faster growth in the long term".

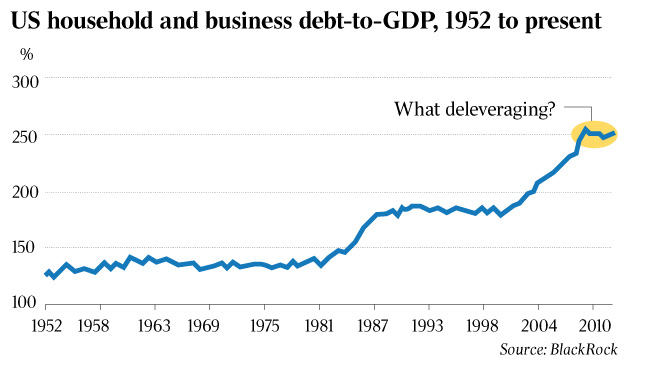

He said most developed countries would suffer this year from the three Ds: "deleveraging, debt and demographics". Although individual investors in the US had sharply reduced their debt since the GFC, the boom in other debt had undone their good work and left non-financial debt (as household and business debt is called) still standing at more than 250 per cent of GDP, "a scant 2 per cent below its 2009 peak".

The ageing population also would be a drag on growth. The good news, however, "is that older people don't borrow as much as younger ones do", thus reducing the risk of potentially inflationary bank lending.

Despite the money printing, "monetary aggregates in the US grew very slowly in the last five years" because of low credit creation (lending) by banks. "That and the lack of wage growth in the US because weak labour markets have kept the risk of inflation pretty low," he said. "This is a good time for institutions to reduce their overweights in the US market back to market weight."

http://www.mckinsey.com/insights/mgi/research/financial_markets/uneven_progress_on_the_path_to_growth

Good spot on the different statistics between BlackRock and McKinsey. Judgement I could make is that U.S. and Australia debt are still very high, which is very very bad.

I don't concern too much about private debt as +Kieran Simpson K is trying to figure out. If you could manage well your personal finance, clean up your own backyard, you won't care too much other people's business unless the grass in your garden is aways greener than the other side.

Public debt is totally different, that is everyone's debt. If you live and work in U.S., your contributed personal tax always have to pay back a bit of public debt. High debt prevents any government to adapt more flexible economic policies.

Lucky we are in Australia, with reasonably sounding economy management government, relatively less government debt than hard condition U.S. and can't-see-future Japan.

Not surprise heard that Britain lose AAA credit rating last week. But it's too bad that news make French happier though France has been striped AAA rating by the same god-damned company Moody :-)